The Ultimate US Tax Calculator Guide: How to Estimate Your Take-Home Pay & Keep More of Your Money

Image Source: Toolilo

Every tax season, millions of Americans ask the exact same question: "Where did my paycheck go?" You negotiate a nice salary, but when the paycheck lands in your account, it looks noticeably lighter. Between Federal withholding, state taxes, and FICA deductions, your hard-earned cash seems to shrink.

Understanding how the tax system works is the first step to optimizing your income. This guide breaks down progressive tax brackets, FICA payroll taxes, and standard vs. itemized deductions, showing you exactly how to estimate your take-home pay and legally lower your tax burden.

A common misconception is that entering a higher tax bracket means your entire income is taxed at that higher rate. People sometimes fear a raise because they think it will drag them into a higher bracket and leave them with less money. Fortunately, that is not how US progressive taxes work.

Think of progressive tax brackets like a series of buckets. As your income increases, it fills up one bucket before spilling over into the next. Each bucket has a different tax rate, and you only pay that rate on the money *inside* that specific bucket.

Here is a summary of the 2024 Federal Income Tax brackets for Single filers:

| Tax Rate | Single Filers Taxable Income Bracket (2024) |

|---|---|

| 10% | $0 to $11,600 |

| 12% | $11,600 to $47,150 |

| 22% | $47,150 to $100,525 |

| 24% | $100,525 to $191,950 |

| 32% | $191,950 to $243,725 |

| 35% | $243,725 to $609,350 |

| 37% | Over $609,350 |

Example: If your taxable income is $50,000, you are in the 22% bracket. However, you do not pay 22% on the full $50,000. Your tax is calculated as:

- 10% on the first $11,600 = $1,160.00

- 12% on the amount between $11,600 and $47,150 ($35,550) = $4,266.00

- 22% on the remaining amount above $47,150 ($2,850) = $627.00

- Total Federal Tax = $1,160 + $4,266 + $627 = $6,053.00

This progressive system is why your Effective Tax Rate (the percentage of total income you actually paid, which is 12.1% in this case) is much lower than your Marginal Tax Rate (22%, which is the tax bracket of your last dollar).

📊 Interactive Bracket Estimator (Try It Out!)

Enter a quick salary to see how it fills the federal tax brackets and what your estimated tax is:

Before taxes are calculated, the IRS allows you to subtract deductions from your gross salary. This gives you your Taxable Income, which is the actual amount subject to tax.

- Standard Deduction

- Itemized Deductions

This is a flat, automatic deduction that requires no receipts or documentation. For 2024, the limits are:

• Single: $14,600

• Married Filing Jointly: $29,200

• Head of Household: $21,900

If you have significant expenses like mortgage interest, charitable donations, or state and local taxes (SALT) that add up to *more* than the standard deduction, you can choose to itemize instead. This requires listing out your expenses when filing, but it can save you thousands if you qualify.

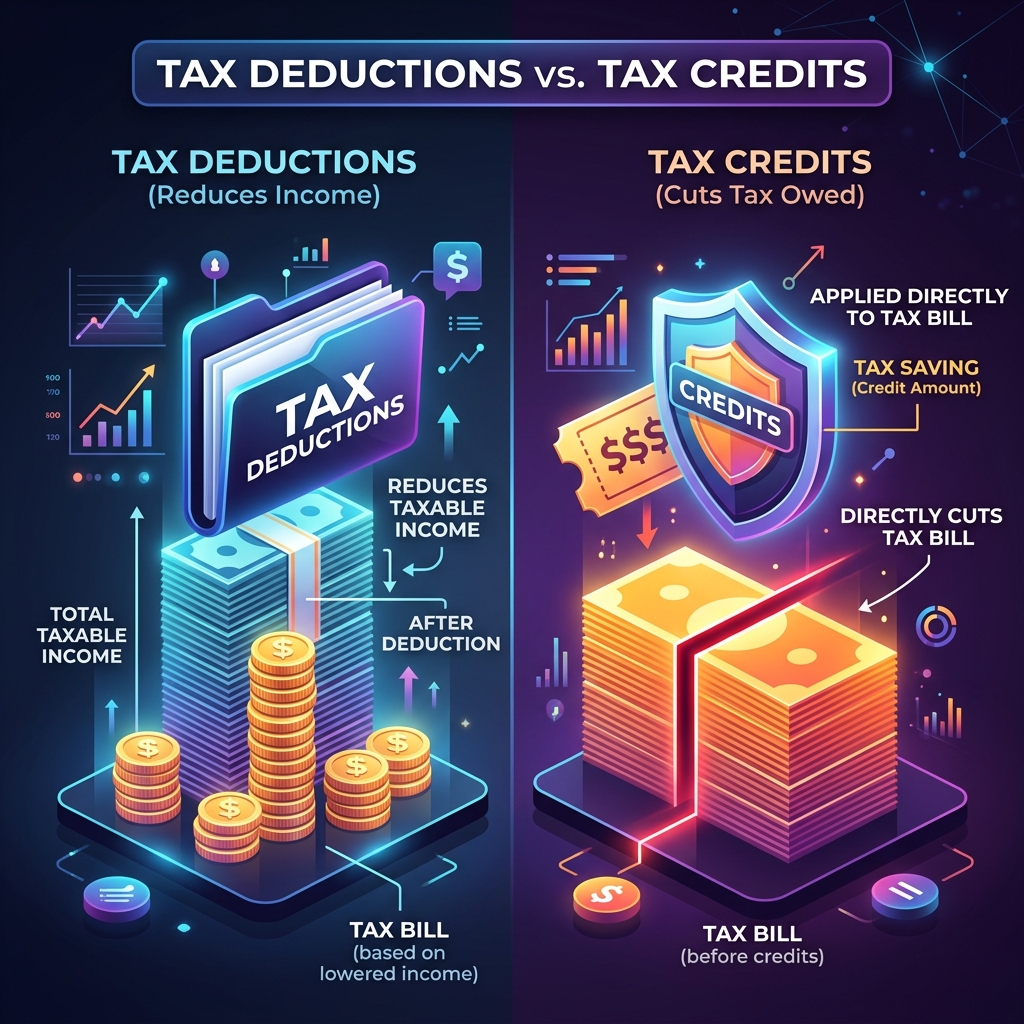

Tax deductions lower your taxable income, while tax credits subtract from your total tax bill dollar-for-dollar.

FICA taxes are separate from income taxes. They are flat-rate taxes that fund federal retirement and healthcare programs:

- Social Security: A 6.2% tax on your wages. However, in 2024, it is capped at a wage base of $168,600. Once you earn above this limit, you pay 0% Social Security tax on the remainder of your earnings.

- Medicare: A 1.45% tax on all wages. There is no cap for Medicare. In fact, if you earn over $200,000 (Single) or $250,000 (Married Joint), you pay an additional 0.9% Medicare surcharge.

How you are employed changes how your taxes are handled. W-2 employees have taxes automatically withheld from their paychecks by their employers. They split FICA taxes with their employers: the employee pays 7.65% and the employer pays another 7.65%.

Independent contractors (1099 workers), however, do not have taxes automatically withheld. They must pay the full 15.3% Self-Employment (SE) tax (the equivalent of both employee and employer FICA portions). On the bright side, 1099 contractors can write off business expenses (home office, internet, software, equipment) to directly lower their taxable business income.

Comparison of tax handling and self-employment tax liabilities between W-2 employees and 1099 self-employed workers.

If you get a massive tax refund, it means you gave the government an interest-free loan. If you owe a lot, you might face penalties. You can adjust your tax withholding by submitting a new W-4 Form to your employer.

By adjusting your filing status, claiming dependents, or entering extra withholdings on the W-4, you can balance your monthly cash flow and ensure your take-home pay matches your actual annual liability.

Now that you know the basics, let's look at simple strategies you can implement today to lower your tax liability:

- Max Out Pre-Tax Accounts

- Utilize a Health Savings Account (HSA)

- Claim All Eligible Tax Credits

Workplace 401(k) and traditional IRA contributions are made with pre-tax dollars. This means the money you contribute is subtracted from your gross salary before the IRS calculates your taxes. For example, contributing $10,000 to a 401(k) directly lowers your taxable income by $10,000, instantly saving you $2,200 if you're in the 22% bracket!

An HSA offers a triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for medical expenses are completely tax-free. If you have a high-deductible health plan, this is one of the most powerful tax shelters available.

Unlike deductions (which reduce taxable income), tax credits are a dollar-for-dollar reduction of your actual tax bill. Look out for the Child Tax Credit, Earned Income Tax Credit, or clean vehicle/energy-efficient home credits when filing.

💸 Interactive Tax Savings Checklist

Select the tax-saving actions you plan to take to estimate your potential tax savings (based on a marginal tax bracket):

Q: What is a progressive tax bracket?

A: A progressive tax system means tax rates increase as your income crosses specific thresholds. You only pay the higher tax rate on the portion of your income that falls within that specific bracket, not your entire gross income.

Q: How can I lower my taxable income?

A: The easiest ways are by contributing to pre-tax accounts (like a traditional 401k, 403b, or IRA), utilizing a Health Savings Account (HSA) or Flexible Spending Account (FSA), and claiming standard or itemized deductions.

Q: What is the difference between a W-2 and a 1099 tax filer?

A: W-2 employees split payroll (FICA) taxes with their employers and have taxes automatically withheld. 1099 contractors pay the entire 15.3% self-employment tax themselves but can write off business expenses to lower their net taxable income.

Q: What is the difference between a tax deduction and a tax credit?

A: A tax deduction lowers your taxable income (saving you a percentage based on your marginal tax bracket). A tax credit reduces your actual tax liability dollar-for-dollar, making credits generally more valuable.

Q: How does the Child Tax Credit work in 2024?

A: For the 2024 tax year, the Child Tax Credit is up to $2,000 per qualifying child under the age of 17. The credit is phase-out based on your modified adjusted gross income (MAGI) starting at $200,000 for single filers and $400,000 for married couples filing jointly.

Q: How can I avoid owing taxes at the end of the year?

A: If you regularly owe money, submit a revised W-4 Form to your employer to increase your federal tax withholding. You can specify a flat extra amount to be withheld from each paycheck to ensure you cover your full liability.

Taxes don’t have to be a black box. By using our interactive Income Tax Calculator, you can play around with different incomes, filing statuses, and pre-tax contributions to see exactly how they affect your tax liability and monthly take-home pay. Start planning today, maximize your contributions, and keep more of your hard-earned money in your pocket.